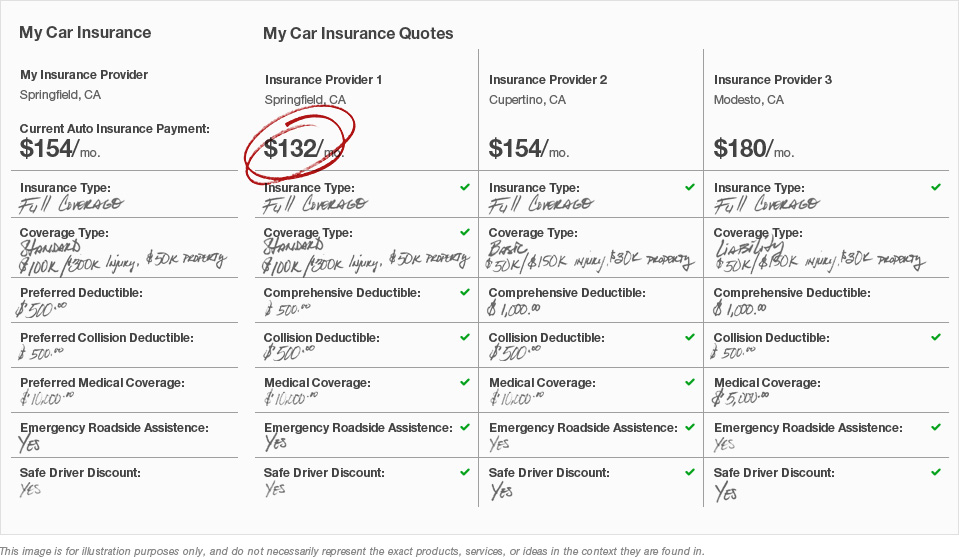

Car Insurance Comparison

In the past few years, insurance providers and independent sites have proliferated online, making the Internet a hypercompetitive market for auto insurance. Radically discounted premiums and higher-quality policies have resulted, both tremendous boons to consumers. Of course, the valuable benefits of a competitive market are entirely lost unless shoppers engage in thorough car insurance comparisons. As you compare auto insurance quote offers, you can more readily see which policies are best-suited for your coverage requirements and personal budget. A car insurance quote comparison also helps you evaluate each carrier for its particular benefits and drawbacks so you end up choosing the company that can accommodate all your needs.

Finding the Lowest Premiums

Every shopper wants to find the lowest premium on his/her auto policy. But in order to know what the lowest possible premium even is for the coverage you desire, you have to complete auto insurance comparisons. Requesting rates from various carriers will give you a better idea of what prices and coverage amounts are reasonable. Best of all, you don't have to undertake an auto insurance quote comparison on your own. If you use our unique quote-retrieval system, we will find and present up to five of the best offers on auto insurance available online at no cost to you.

![[X] (click to close)](/images/x_close.png)