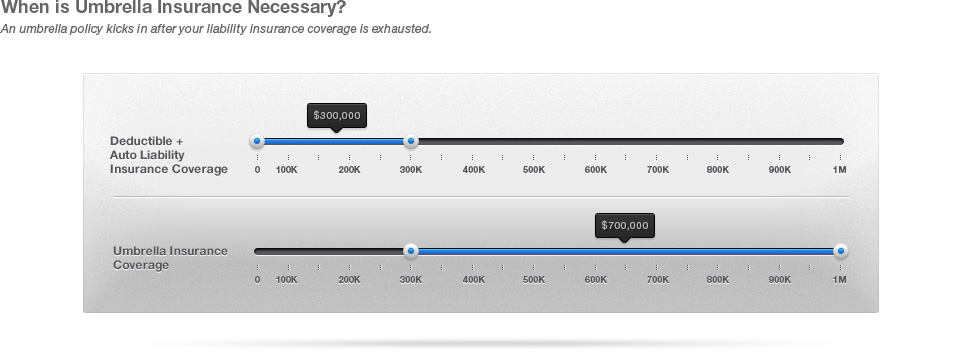

Umbrella Liability Insurance Coverage

For many policyholders, the highest-available payment limit on the liability coverage of their home or auto insurance is still insufficient. On most policies, the largest limit offered is $300,000, which would only suffice if the value of policyholder's assets fell below that figure. Otherwise, one costly money judgment against the policyholder could jeopardize his/her assets once the liability coverage is exhausted. To avoid winding up in such a situation yourself, you might consider augmenting your auto or home insurance with umbrella insurance coverage.

What Is an Umbrella Policy?

The best way to explain umbrella coverage is by way of example. The following scenario is illustrative of both the nature and necessity of umbrella insurance coverage. Imagine you lose control of your car and crash into a late-model Jaguar driven by a wealthy surgeon. He's injured so badly in the accident that he is unable to work ever again. He sues you, and the jury returns a verdict in his favor with a multi-million-dollar award. The limit on your auto liability insurance was $300,000, so the court seizes your savings, garnishes your salary for years to come, and goes after your house to make up the difference.

Had you carried umbrella liability coverage in the aforementioned scenario, your umbrella policy would have been triggered as soon as you met the $300,000 deductible, which was satisfied by your auto liability coverage. Your insurer would not only have covered the judgment against you, but also would have furnished a legal team to defend you. An umbrella policy would have supplemented your auto liability coverage and protected your assets against the large judgment.

Who Should Purchase Umbrella Liability Coverage?

A popular myth is that only the uber wealthy need to purchase an umbrella liability policy. In reality, you do not need a great deal of wealth for your assets to potentially be in jeopardy without proper liability coverage. Assuming you select the highest payment limit on your auto liability policy, you would only need to have assets in excess of that limit, typically $300,000, to justify umbrella insurance coverage. If you own a home and a car, have investments, and/or have accumulated a retirement nest egg, it's not difficult to exceed the $300,000 threshold. Essentially, if the value of your assets less your liabilities (debts) exceeds your maximum liability coverage, you should purchase an umbrella policy.

How Much Coverage to Buy

Most carriers offer umbrella liability policies ranging in value from $1,000,000 to $10,000,000. While those numbers may seem high, insurance experts will tell you that most people who carry umbrella insurance coverage actually don't carry enough. To decide on the right amount for you, add up your salary, your home equity, the value of your real property (e.g., jewelry, vehicles, land, etc.), your investments and savings, and the value of your business, if applicable. Subtract your debts from that figure to arrive at your net worth. From that number, subtract the payment limit on your auto liability policy to determine how much coverage you should buy.

![[X] (click to close)](/images/x_close.png)